Dollar cost averaging is a popular method for long term investment either in stock, unit trust and etc. Through this technique, you need to make monthly installments at a certain amount.

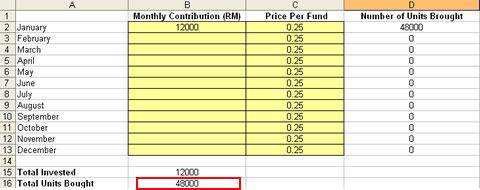

For example, let say you have RM12,000 to invest in unit trust and you are not using dollar cost averaging, then you will simply invest the entire amount at one time and let it stay there for 1 year and gain profits after that.

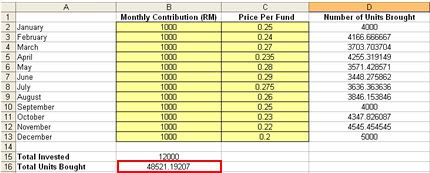

On the other hands, if you are using dollar cost averaging, then your amount RM12,000 will be break down into 12 months(which equivalent to 1 year). So, you have committed to invest RM1000 per month:

Why dollar cost averaging will benefits us? This is because the amount that you invested every month will be fixed usually but the fund price will be varied which either high or low; thus you will be purchasing more funds if the price is low and less amount of fund if the fund price is high.

I have created the calculation of dollar cost averaging method using an Excel spreadsheet. Click it here.

Different Between Dollar Cost Averaging and Lump Sum Investment

Somebody had asked me before, what’s the different between one lump sum investment and dollar cost averaging method. What do you think? Which one will give better result?

Actually both methods also can be used and it depends on how you manage your money. For those who do not prefer to time the direction or always monitor the fund, then choosing the dollar cost averaging method will be the most suitable for them as they can purchase more units of fund at the markets bottom.

My personal tips for you: Your investment strategy should take into consideration the risk that you’re willing to take. If you worry that your fund prices would immediately drop after your initial investment, then it’s advisable to go for dollar cost averaging method.

Comparison as such between lump-sum and dollar-cost-averaging is indeed biased, only tells half of the story. It is only good to be used by “sales profesionals” to “mislead” potential customers.

While the lump-sum RM12000 could be invested at the very beginning for a price of RM0.25 (getting 48000 units then), it has EQUAL chance/probability to have been invested at the lowest price of all, that is RM0.20, thereby getting 60000 units !!! Again, look at the dollar-cost-averaging, getting a total of 48521.19 units: dollar-cost-averaging, when “wins”, only wins a mere 521.19 units; but when “loses”, loses a 11478.81 units !!!

Some may argue it’s because the price RM0.20 is chosen, but why he is not asking why RM0.25 is chosen for the comparison in the first place then ??!!