A nominal rate of return is also called gross rate of return. The real rate of return is simply the gross return less inflation. Do you think is it better to use real returns or nominal returns for your future projections?

Due to the inflation changes the money value, so the investment value of RM100,000 today is totally different it was 20 years ago.

When I plan for my retirement savings, I always use real rates of return with an inflation rate of x%. The reason is to make the numbers more understandable. Let’s take an example:

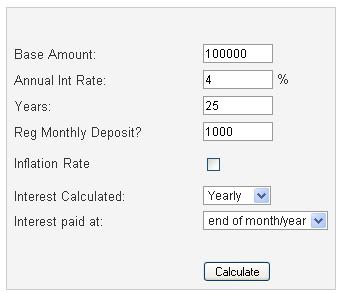

Michael and Jackson are 30 years old and want to retire in next 25 years. Let say they own RM100,000 in investments and are able to put away RM1000 per month. If we assume a nominal rate of return of 8% and an inflation rate of 4%, how much they will have at retirement age?

Real Interest Rate = Nominal Rate – Rate of Inflation

If we use the nominal return approach, they will have RM 1,632,300.50 in 25 years. But, if we use the real rate of return approach, then they will have RM 786,324.57 in 25 years. There’s difference of RM845,976. So, no matter which approach you use, you need to account for inflation in your retirement planning. If you use nominal returns, then you have to factor inflation.