Do you think investment through property rental can guarantee you to earn higher return in the long run if compare to fixed deposit saving? Anyway, you should make a proper plan before buying any property for investment.

Based on my understanding, if buying a house now, then for sure the price will go up. But, will you really earn? You need to know that some of the money have to be paid to bank interest first and also you might spend some money to renovate your house and other expenses like maintenance fees for the house.

How to Calculate Return On Investment for Property Rental?

Property Type: Apartment

Size: 650 square feet

Housing Price: RM 75,000

Down Payment: RM 7,500

Housing Loan Amount: RM 67,500

Loan Interest Rate: 5% (assumption)

Loan Tenure: 15 years (assumption)

Housing Loan Installment: RM 534 per month

Gross Rental: RM 600 per month

Other Expenses: Maintenance fees and renovation cost

Monthly Net Rental = Gross Rental – Loan Installment

= RM 600 – RM 534

= RM 66

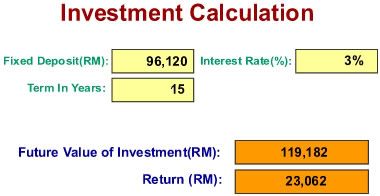

Fixed Deposit vs Property Investment

Fixed Deposit (with 3% interest rate) => return is RM 119,182 – RM 96,120 = RM 23,062

Property Investment (with BLR-0%) => return is Gross Rental – Loan Installment = RM 66 monthly

This figure is enough to cover low cost apartment maintenance fees. But it’s risky, as you might not rent to anyone within 15 years. However, you own the ownership on the property with the initial down payment of RM 7,500. That means your RM 7,500 has became RM 75,000(if continuing rent without fail). Here, I made another worst assumption that your property value is maintaining at same price after 15 years. Normally it less likely will happen. After minus initial renovation cost, you still earn more than double of fixed deposit saving.

So, can you see the different between fixed deposit vs property investment?

I think the comparison is over simplified for a number of reasons:

– time value is not considered

– not comparing apple to apple (i.e. comparing a person who has $7500 (down payment) vs someone who has $75000 FD)

I can’t comment on other assumptions, such as $600 rental income, no maintenance cost, etc.

FD is passive income, property investment is usually an active income in order to earn much higher income with assurance. so, earn money using property, then save the profit in FD or other passive income generator to rip benefits from both sides.

Sorry… I still cannot get the point. How does RM 96,120 come from?

Hi DavidLee, Long time since I’ve been over here but that’s my bad. Now I’m here and you have an interesting post but the math part of it is a little too much for this brain of mine. I do own property that my sister & I inherited and we have been hanging onto it until the Market was a little bit better. Now is the time for us to start to think about the selling of it or do we want to hang on to it and rent it out? So we do have two options but with this economy who knows which way is the best. I’m sure your formula is great, but I think probably property would be better than savings- I have no idea. Thanks for the info. jj

I not much bullet go for property investment yet

something came across my mind exactly today..

be4 that, can we get an apartment now with only 75K? I’m still doubt that..

the comparison u made were based on FD and property investment ..

in this case, i shall agree to property investment..

but what if I invest on ASM or any unit trust by government with a return of minima 6 % and above and compare with property investment?

i really hope u can make such comparisons..

a rough idea is that given 100 K into ASM is more profitable than using 100 K in property investment..

if ASM, i can get rm 6800 per year(if interest rate is 6.8%)

if house rental i can get rm 7200 per year (if monthly rental is rm 600).

For apartment, we need to pay the maintenance, the indah water, the dbkl, renovation and etc..

i am sure with ur knowledge u can justify better than me. hope to hear the reply

@spBlogger: RM96,120 is came from Rm534 monthly FD saving

@jj-momscashblog: sometimes the formula can really help people to think properly and make wise decision.

property is definitely better than fd

Is the rental you mean in KL?

If PG, rm600/month for a low cost apartment is too idealistic. Normally they only manage to rent out at rm400 for 600+sqf 3 rooms.

Maintenance rm50-80/month.

For property investment, normally the total of 10 months rental should cover your 12 months of housing loan. The rest use for the quick rent, insurance, maintenance and repairing cost.

Nevertheless, investment and FD cannot be compare. You should compare different type of investment, but not comparing saving vs investment.

wow….good write up….as for me, i love property ivnestment but it is a big risk…if u invest in a wrong property…datsit…u r tied and bounded for life unless u can sell for profit.

I have no control over investments (public mutuals, bonds etc) and i have more control over property investment (location, renting, selling)

Thus, more into property investing rather than fixed deposit.

i believe if one follow some investment rule in property such as buying a house or shop. one can actually acquire a piece of property for free or almost free. and size of the house to own depend on how capable in you to manage it.

yes I agree Property really is safe investment. Right calculation is important before deciding to invest.

I got a good link which gives guidelines for our investment in real estate. Hope this will help you

http://www.commonfloor.com/articles/popular-methods-to-calculate-maintenance-fee-in-apartment-complexes-505.html

i suppose FD is hassle free while property investment may generate a better return only if your property is located at a prime location. Why not consider an investment in land instead? It is a low risk middle term (4-6years) investment that can yield a return of 15% p.a. Only catch is you need at least RM35k to start.

If any of you are interested in the details you can always drop me a mail at nkweng@hotmail.com.

Bros,

Does anybody know what the darn is tax deffered exchange??? the one that they call 1031??

Good illustration…In my point of view, these instruments carrying different level of risks. FD can be considered risk-free while the volatility in property market is definitely higher.

The second point irefer to the liquidity of both instruments. FD is highly liquid as it can be withdraw from you bank account at any time (may you have to sacrifice some interest). So, the return of FD is also lower. However, it is totally different for property. Property is less likely to dispose off in a short period. Sometimes you even have to sell at below market price. Therefore, the return in property investment is higher than FD due to differential in volatility and liquidity.

Anyway, i appreciate your valuation in these investments =)

How about other fees like S&P agreement legal fees, bank loan agreement legal fees, MRTA, valuator fees and etc? Should be taken into account on top of the 10% down payment. It’s not that easy like that you said.

I would prefer investment into REIT by leveraging on the same kind of housing loan (if available, since interest is just BLR-2.x%, which is about 4.x% now) and yet, I can again about 7-8% in return.

Very nice article on investment calculation…It clearly states that Property investment is always better than fixed deposit.I agree with you.